Is 65 the right time for you to sign up for Medicare? It depends, but if you do, please note that your income will determine your Part B and possibly Part D premiums.

Seniors 65 or older can sign up for Medicare. The government refers to people who receive Medicare as “beneficiaries.” Medicare beneficiaries must pay a premium for Medicare Part B (outpatient services), which covers doctors’ services, outpatient surgery, labs, and x-rays, and Medicare Part D, which covers prescription drugs. The premiums paid by Medicare beneficiaries cover about 25% of the program costs for Part B and Part D. The government pays the remaining 75%.

What Is IRMAA?

Medicare imposes surcharges on higher-income beneficiaries. The theory is that higher-income beneficiaries can afford to pay more for their healthcare. Instead of doing a 25:75 split with the government, they must pay a higher share of the program costs.

The surcharge is called IRMAA, which stands for Income-Related Monthly Adjustment Amount. This applies to both Traditional Medicare (Part B and Part D) and Medicare Advantage plans.

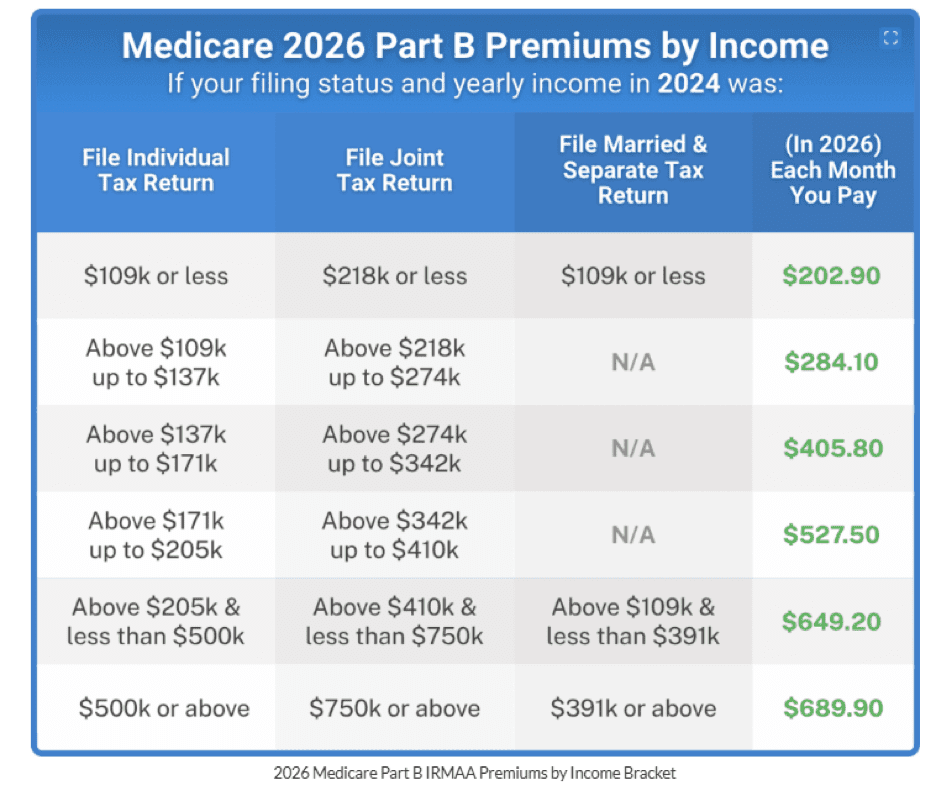

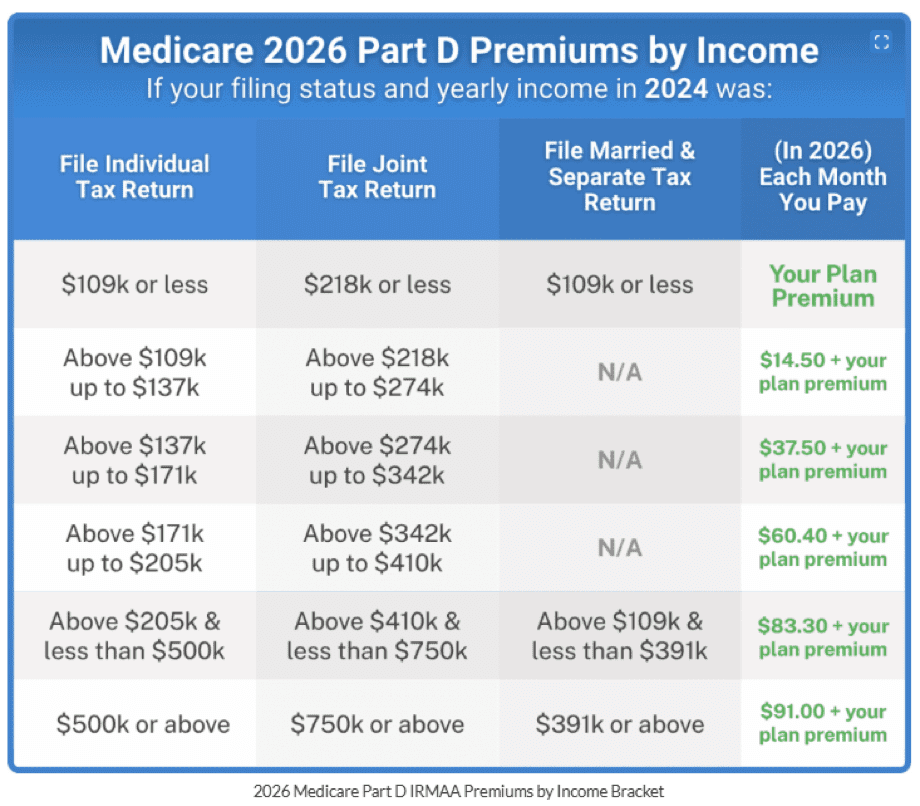

Here are the IRMAA brackets for 2026.

Important note: IRMAA brackets are treated as a “cliff” – once you are $1 over the threshold for that bracket, you are bumped into the higher premium payment (e.g., $109,001 in Modified Adjusted Gross Income places you into the 2nd bracket – $284.10 Part B and $14.50+ your plan premium).

https://boomerbenefits.com/new-to-medicare/medicare-cost/

MAGI

The income used to determine IRMAA is your Modified Adjusted Gross Income (MAGI) — which is your AGI plus tax-exempt interest and dividends from muni bonds — from two years ago. Your 2023 MAGI determines your IRMAA in 2025. Your 2024 MAGI determines your IRMAA in 2026. Your 2025 MAGI determines your IRMAA in 2027.

The MAGI for IRMAA includes taxable Social Security benefits, but it doesn’t include untaxed Social Security benefits. If you read somewhere else that says that untaxed Social Security benefits are included in MAGI, they’re talking about a different MAGI, not the MAGI for IRMAA.

IRMAA Appeal

If your income two years ago was higher because you were working at that time, and now your income is significantly lower because you retired (“work reduction” or “work stoppage”), you can appeal the IRMAA initial determination. The “life-changing events” that make you eligible for an appeal include:

- Death of spouse

- Marriage

- Divorce or annulment

- Work reduction

- Work stoppage

- Loss of income from an income-producing property

- Loss or reduction of certain kinds of pension income

You file an appeal with the Social Security Administration by filling out the form SSA-44 to show that although your income was higher two years ago, you have a reduction in income now due to one of the life-changing events above. For more information on the appeal, see Medicare Part B Premium Appeals.

Not Penalized For Life

If your income two years ago was higher and you don’t have a life-changing event that makes you qualify for an appeal, you will pay the higher Medicare premiums for one year.

IRMAA is re-evaluated every year as your income changes. If your higher income two years ago was due to a one-time event, such as realizing capital gains or taking a large withdrawal from your IRA, your IRMAA will come down automatically when your income comes down in the following year.

Planning Ahead

This is why it’s important to understand the series of irreversible decisions in retirement. IRMAA-related charges are part of the ongoing series of irreversible decisions in retirement. Every year, once you are 65 and over, whatever you showed in income 2 years ago will impact your premiums on Part B and D this year. This is why it’s important to plan out how much gross income you show during the year, utilizing Roth, cash, and other vehicles to stay under the next bracket.

This blog was co-authored by:

Sharon Accardo, Medicare Expert, sharon@thinkinnovative.net , and

Albert Wu, Certified Financial Planner ® albert.wu@vocarewealthadvisors.com

Any opinions are those of Vocare Wealth Advisors and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. Raymond James and its advisors do not offer tax or legal advice. You should discuss any tax or legal matters with the appropriate professional. Investing involves risk and you may incur a profit or loss regardless of strategy selected, including diversification and asset allocation. Prior to making an investment decision, please consult with your financial advisor about your individual situation.