How to Choose the Right Financial Advisor: 10 Questions That Matter

If you’re approaching retirement—or facing major financial decisions—you want more than investment management.

You want clarity and thoughtful guidance from someone you trust who understands the life you’ve worked hard to build.

You’ve likely spent decades building your career, saving consistently, and making responsible decisions. But as retirement approaches, the questions change—and the stakes feel higher.

This stage of life is no longer just about growing assets. It’s about coordinating everything you’ve built so it works together.

If you’re interviewing financial advisors and trying to understand who you can truly trust, this guide is designed to help you ask better questions and listen for better answers.

The goal is not to find the “best” advisor in general. It’s to find the right advisor for your situation.

What Selecting the Right Financial Advisor Really Means

Choosing a financial advisor is not about finding someone who promises the highest returns.

At this stage of life, it’s about judgment.

It’s about finding someone who:

- Understands your full financial picture

- Removes their own incentives from shaping your decisions

- Coordinates income, taxes, healthcare, investments, risk, estate planning, and lifestyle into one coherent strategy

When you’re no longer accumulating, mistakes are harder to recover from, and opportunities are easier to miss.

The wrong advisor may not make obvious mistakes, but they may narrow your options or miss how decisions ripple across your plan.

The right advisor brings clarity to the full picture, names trade-offs, and helps you move forward with confidence.

Why This Decision Matters More Than Most People Realize

Many financial mistakes are not caused by bad markets. They are caused by poor guidance.

Decisions around:

- Retirement timing

- Social Security

- Tax strategy

- Risk exposure

They are often irreversible or costly to unwind.

An advisor who focuses too narrowly on one area, or whose recommendations are shaped by incentives rather than understanding, can limit your options.

That’s why choosing the right advisor matters just as much as the plan that follows.

A Framework for Evaluating Financial Advisors

Many people assume the best advisor is the one with the most impressive credentials, the strongest marketing, or the most confident answers.

In reality, the right advisor is revealed through how they think, how they make decisions, and how their incentives align with yours.

Good advisors are not identified by what they claim. They are revealed by how they answer thoughtful questions.

This guide uses ten questions to help you evaluate:

- How an advisor thinks

- How they are incentivized

- How they work with clients

Each question is designed to reveal behavior, not just promises.

Key Takeaways (Read This Before You Start Interviewing)

- Choosing a financial advisor is not about finding the highest returns. It’s about finding good judgment, aligned incentives, and a process that protects your options.

- No compensation model is conflict-free. What matters is whether an advisor acknowledges incentives and manages them transparently.

- Fiduciary is a standard, not a guarantee of behavior. Two advisors can both claim to be fiduciaries and still act very differently.

- Advisors who exclude entire categories of solutions before understanding your situation may be limiting outcomes and not acting in your best interest.

- Good advice slows decisions down. Pressure, urgency, or overly simple answers are warning signs.

- The right advisor helps you see trade-offs clearly and decide with confidence, not certainty.

Interview Questions

Do you follow a fiduciary standard—and How Do You Demonstrate That in Practice?

This is the most common question people ask—and it’s an important one. But it is not enough on its own.

Anyone can say “yes” to being a fiduciary. What matters is whether their behavior consistently reflects it.

A true fiduciary standard removes the advisor’s self-interest from the decision-making process and prioritizes what is right for the client—even when it conflicts with how they are paid, what they prefer, or what is easiest.

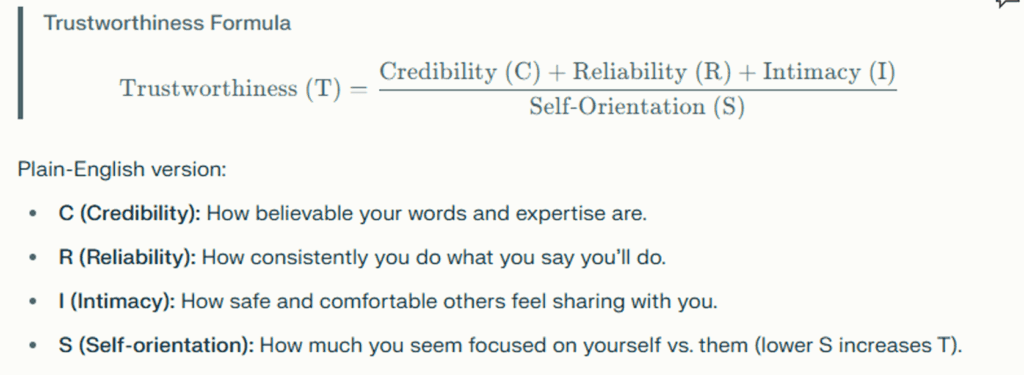

One useful way to think about trust comes from Robert M. Galford’s The Trusted Advisor. Trust is based on:

- Credibility

- Reliability

- Intimacy

- Low self-orientation

Self-orientation is in the denominator of the equation for a reason; it is the biggest variable in determining a person’s trustworthiness.

An advisor who is highly self-oriented tends to:

- Fixate on their way of doing things.

- Push familiar solutions before fully understanding your situation.

- Narrow options prematurely

You should pay attention to how you feel during the conversation. Are they listening deeply, or steering quickly?

A note on “fee-only” and other buzzwords

There has been a growing trend in the industry to treat “fee-only” as synonymous with “fiduciary.” That is a mistake.

Just because someone is fee-only does not automatically mean they will act as a true fiduciary in practice. You cannot determine fiduciary behavior solely based on whether an advisor uses or avoids certain products or services.

An entire segment of the industry has built its moral superiority on refusing to use products X, Y, or Z. That does not eliminate conflicts; it simply changes them.

This would be like a doctor who only prescribes medication and never considers physical therapy, lifestyle changes, or surgery—regardless of the patient’s condition.

That doctor could still claim they are acting in the patient’s best interest. But by limiting treatment options, they are effectively steering the outcome. True care starts with understanding the patient. The treatment follows.

The same is true with financial advice. A true fiduciary doesn’t start with the tool. They start with the problem.

Why incentives matter

An advisor charging 1% of assets under management may be disincentivized to recommend an annuity, or to pay off a mortgage —even if it fits a client’s low risk tolerance—because it removes assets from the portfolio and thereby reduces ongoing revenue for the advisor.

Conversely, an advisor focused exclusively on using annuities may ignore other tools such as cash, bonds, CDs, stocks and index investments, because those don’t fit their business model and their incentive structure.

Neither structure is inherently good or bad. What matters is whether the advisor:

- Understands your goals and concerns

- Presents multiple viable solutions

- Explains the pros and cons of each

- Helps you choose what fits your risk tolerance and priorities

Do they diagnose before prescribing?

If an advisor recommends a solution before fully understanding your goals, concerns, and constraints—especially a one-size-fits-all approach—that should give you pause.

There is no universal “good” or “bad” product. Any advisor who categorically rejects entire categories of solutions is leaving options off the table that may be appropriate for certain clients.

How Do You Get Paid?

Most people don’t realize they are choosing both a financial advisor and a business model at the same time.

How an advisor is compensated does not automatically determine the quality of their advice—but it does shape incentives.

Understanding those incentives helps you recognize where blind spots or conflicts could arise.

Most advisors operate under one of four primary compensation models:

1. Assets Under Management (AUM)

How they’re paid:

A percentage of the assets they manage for you.

What it does well:

Investment management, portfolio construction, and behavioral coaching during market volatility.

Where incentives can influence advice:

Because compensation is tied to assets under management, advisors may be less inclined to recommend strategies that reduce those assets—such as paying off debt, gifting assets, purchasing annuities, or increasing lifestyle spending in retirement.

2. Flat-Fee or Advice-Only Planning

How they’re paid:

A flat annual fee, subscription, or project fee that is not tied to investment assets.

What it does well:

Comprehensive financial planning, tax strategy, retirement income planning, Social Security, and Medicare decisions.

Where limitations may exist:

Implementation is often left to the client. Investment management may be limited or optional, requiring a more hands-on role from the client.

3. Insurance-Focused Advisors

How they’re paid:

Commissions from insurance products such as annuities, life insurance, or long-term care policies.

What it does well:

Risk management and guaranteed income strategies.

Where incentives can influence advice: Recommendations may center on the products the advisor is licensed to sell, sometimes limiting consideration of traditional investments such as stocks, bonds, or index funds.

4. Transaction Commissions

How they’re paid:

A commission each time a financial product or investment is bought or sold.

What it does well:

This model can be appropriate for investors who only need occasional transactions or one-time product purchases rather than ongoing advice.

Where incentives can influence advice:

Because compensation is tied to transactions, advisors operating under this model may have an incentive to recommend trades or products more frequently. Ongoing planning, tax strategy, or retirement coordination may receive less attention if the relationship centers primarily on transactions.

How Do You Approach Proactive vs. Reactive Planning?

Good planning anticipates change.

The difference between proactive and reactive advice often shows up in whether conversations happen before or after a costly decision.

Tax laws, markets, healthcare rules, and estate laws evolve constantly. Waiting until something happens to react often means opportunities have already been missed.

Proactive planning means identifying potential issues before they become problems—and adjusting your strategy along the way.

For example, many retirees discover too late that their retirement income affects far more than taxes. It can also influence Medicare premiums, Social Security taxation, Required Minimum Distributions, and eligibility for certain deductions or exemptions.

An advisor who plans proactively helps you think through these interactions before decisions are locked in.

When evaluating an advisor, ask how they:

- Stay ahead of tax law changes

- Prepare clients for market downturns

- Review tax strategies before year-end

- Revisit assumptions as circumstances change

Follow-up questions might include:

How has your advice changed due to recent tax law updates?

How did you help clients adjust their plans after laws such as SECURE 1.0, SECURE 2.0, or other recent tax legislation?

How do you help clients:

- Avoid probate?

- Reduce taxes and penalties?

- Prepare for bear markets?

- Plan for Medicare and healthcare costs?

Listen carefully for whether the advisor describes a process or simply general intentions.

How Are You Meaningfully Different From Other Advisors?

Be cautious if the primary differentiator is investment performance.

Sustainable differentiation usually comes from:

- Experience with your specific situation

- Perspective

- Planning depth

Ask whether they regularly work with people in situations like yours and whether their advice extends beyond investments.

How Deep Does Your Planning Go?

This reveals whether the advisor is managing portfolios or guiding decisions.

Ask:

- What does a comprehensive plan include?

- How are taxes, insurance, estate planning, and cash flow integrated?

- How do you coordinate with my CPA and attorney?

- How often is the plan revisited?

Planning should be an ongoing process, not a one-time document.

How Do You Select Investment and Insurance Recommendations?

Some advisors are limited to proprietary products. Others have open access.

Ask:

- What constraints exist?

- How do those constraints affect recommendations?

Limitations don’t make someone unethical—but they do matter.

What Types of Clients Do You Specialize In?

Advisors, like doctors, develop specialties. Relevant experience matters.

Ask:

- Who is your ideal client?

- Who are you not a good fit for?

- Can you share examples of clients with challenges like mine?

Which Other Advisors Do You Respect? And Why?

This question reveals confidence and professionalism. Advisors who learn from peers and welcome comparison tend to be more secure in their approach.

How Do You Help Clients Decide When They Can Retire?

Many advisors are trained primarily for the accumulation stage of life—helping people grow assets over time. Retirement introduces a very different challenge: turning those assets into reliable income while managing taxes, healthcare costs, and market risk.

This stage, often called the decumulation phase, requires a different skill set.

Many people reach a point where they can retire on paper—but still feel uncertain about whether they should.

Listen carefully to how an advisor addresses:

Income planning – How do they structure income to replace your paycheck in retirement?

Social Security strategy – Do they explain not only when to claim benefits, but why that timing fits your broader plan?

Emotional readiness – Do they discuss the transition away from work and how retirement changes spending patterns, structure, and lifestyle?

Tax coordination – Retirement income affects more than your tax bracket. It can influence IRA and 401(k) distributions, Medicare premium surcharges, deductions, and certain exemptions. Small decisions about where income comes from can ripple through your entire plan.

Helping someone confidently say “yes” to retirement requires more than running projections. It requires coordinating income, taxes, healthcare, and lifestyle decisions into a plan that can hold up over time.

What Does the Ongoing Relationship Actually Look Like?

Ask:

- How often do we meet?

- Who sets the agenda?

- Who do I work with day-to-day?

- What decisions do you proactively help with?

Vagueness here is a warning sign. You want to know what processes and systems the advisor has in place to increase the probability of a successful outcome.

These 10 questions will help you get to the bottom of how the advisor thinks, their business model, and any potential conflicts of interest.

We recommend using this guide as a framework, not a checklist.

The right advisor will welcome these questions and slow the process down. If you leave meetings feeling pressured, rushed, or confused, keep interviewing.

If you leave feeling heard, clearer, and more confident about the path forward, you may have found the right fit.

The goal is not perfection; it is alignment.

Frequently Asked Questions

What does “fiduciary” really mean in practice?

Fiduciary means having a legal obligation to act in the best interest of the other party. In practice, fiduciary behavior shows up in how advice is given, not just in the label. A fiduciary diagnoses before prescribing, explains multiple viable options, discusses trade-offs openly, and is willing to recommend solutions that may not maximize their own compensation. A true fiduciary is also willing to tell you they are not the right fit to help you if their approach does not align with your best interest.

Is “fee-only” automatically better than other compensation models?

No. Fee-only reduces certain conflicts but introduces others. Advisors paid as a percentage of assets under management may be disincentivized to recommend strategies that reduce those assets (e.g., paying off a mortgage, gifting money, or spending additional money on travel). The real issue isn’t the model—it’s whether the advisor is transparent about incentives and willing to put the client’s interests first when trade-offs arise.

Are annuities always bad?

No. Annuities are tools. In some situations, they can provide valuable income stability or risk reduction. In others, they may be inappropriate or unnecessarily expensive. An advisor who categorically rejects or pushes annuities without first understanding your goals is starting with the tool instead of the problem.

How many financial advisors should I interview?

There’s no fixed number, but most people benefit from speaking with at least two or three. The goal isn’t to find consensus—it’s to notice differences in judgment, process, and how each advisor makes you feel about the decisions ahead.

What are red flags during an advisor meeting?

Common red flags include:

- Feeling rushed or pressured to act

- Being funneled toward a single “obvious” solution

- Avoidance of discussing conflicts or downsides

- Overconfidence without nuance

- A heavy focus on products or performance before understanding your situation

Is investment performance a good way to evaluate an advisor?

Investment performance is easy to market but difficult to evaluate in context. Retirement outcomes are driven more by income planning, tax coordination, risk management, and decision timing than by outperforming a benchmark. Strong performance does not automatically equal good advice.

What should a good ongoing advisor relationship look like?

A good relationship is structured and proactive. You should know how often you’ll meet, what decisions the advisor helps with, how changes are anticipated, and what success looks like over time. If this is vague, expectations are likely to be misaligned.

What if I still feel uncertain after meeting with advisors?

Uncertainty doesn’t mean you’re unprepared. It often means the advice hasn’t been clear or complete. The right advisor helps convert uncertainty into clarity—not urgency.

Post Interview Assessment

Download Our Post

Interview Assessment

Download Our Post

Interview Assessment

This guide is designed to help you evaluate advisors objectively—not based on charisma, promises, or pressure.

When a Second Perspective Can Help

If you are interviewing multiple advisors and want help interpreting what you’re hearing, identifying blind spots, or understanding trade-offs that may not have been fully explained, Vocare can help.

We often serve as a sounding board and second opinion for individuals who want to make the right decision—not the fastest one.

Our role is not to sell products or rush decisions. We help people approaching retirement bring clarity to the decisions that matter most: retirement income, taxes, healthcare costs, investment risk, estate planning, and timing.

If You’d Like to Talk

If you’d like a second opinion on your situation or want to understand whether you’re truly on track to retire when you think you are, we offer a complimentary conversation designed to provide clarity, not pressure.

Our goal is simple: to help you retire with confidence, clarity, and purpose.

The Vocare Wealth Advisors Team

Any opinions are those of the author and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Past performance is not a guarantee of future results. Investing involves risk and you may incur a profit or loss regardless of strategy selected, including asset allocation and diversification.

This material is being provided for informational purposes only and is not a complete description, nor is it a recommendation. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Any opinions are those of the author and not necessarily those of Raymond James. All opinions are as of this date and are subject to change without notice. Prior to making a decision, please consult with your financial advisor about your individual situation.

In a fee-based account, clients pay a quarterly fee, based on the level of assets in the account, for the services of a financial advisor as part of an advisory relationship. In deciding to pay a fee rather than commissions, clients should understand that the fee may be higher than a commission alternative during periods of lower trading. Advisory fees are in addition to the internal expenses charged by mutual funds and other investment company securities. To the extent that clients intend to hold these securities, the internal expenses should be included when evaluating the costs of a fee-based account. Clients should periodically re-evaluate whether the use of an asset-based fee continues to be appropriate in servicing their needs. A list of additional considerations, as well as the fee schedule, is available in the firm’s Form ADV Part 2 as well as the client agreement.