Controlling your adjusted gross income in retirement can have 2nd and 3rd order consequences impacting taxes, Required Minimum Distributions, Medicare premium surcharges (IRMAA), and how much your heirs pass in taxes when you pass.

Understanding how your various accounts affect your Adjusted Gross Income (AGI) each year is important. You control how you distribute funds from your accounts, and therefore how much AGI you report on your tax return each year.

You probably already know about the age 59 ½ rule. If you draw from these accounts before 59 ½, a 10% penalty applies in addition to any taxes you owe for the distribution. There are some nuances to this rule for Roth accounts, which are explained in the Roth section of this article, but for pre-tax balances, a 10% penalty applies to every dollar you withdraw before age 59 ½.

There are two exceptions to this rule, which we cover below for pre-tax balances.

Here are the common accounts that most Americans have by the time they retire:

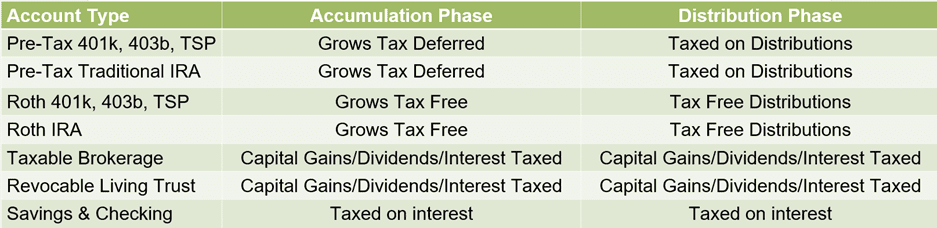

Pre-tax 401(k), 403b, and TSP Accounts

Grow tax deferred. The capital gains, interest, and dividends while held in these accounts are not taxed. However, upon distribution after 59 ½, every $1 is taxable in the same way a W-2 income is taxed for federal and state income taxes. If you distribute $100k from 401(k), 403b, or TSP, it will count as $100k towards your adjusted gross income.

Traditional IRA Accounts

Traditional IRA accounts also grow tax-deferred. Assuming you have no after-tax contributions to your Traditional IRA and all your Traditional IRA is “before tax”, then this account acts the same way as your 401(k), 403b, and TSP. The capital gains, interest, and dividends while held in these accounts are not taxed. However, upon distribution after 59 ½, every $1 adds to your adjusted gross income calculation.

Pre-tax 401(k), 403b, TSP, and Traditional IRA accounts are all subject to Required Minimum Distributions (RMDs). To calculate how much you owe when you reach RMD age, you take the aggregate balance of these accounts and divide it by the factor provided by the IRS.

An exception to the RMD rule? If you are still working during your RMD years, your 401(k) at your current employer is not subject to RMDs. So if you love work and can’t see yourself retiring anytime soon, you could roll your pre-tax IRA, 401(k), 403b, and TSP balances to your current employer’s 401(k) and avoid RMDs on all of the pre-tax balances. Take note: if you own 5% or more of the company you are currently working for, the RMD exception does not apply; your 401(k) will be subject to RMDs.

Exception for Traditional IRAs to the 59 ½ rule

For a traditional IRA, the 60-day rollover rule says: if you take money out and want to keep it tax-deferred, you generally have 60 days to put the same amount into another IRA (or back into the same IRA).

Here are the key points:

Basic mechanics

- You receive a distribution from a traditional IRA, payable to you personally (a check or deposit).

- From the date you receive the money, you have 60 days to redeposit (roll over) that amount into the same or another traditional IRA.

- If you complete the rollover within 60 days and follow the other rules below, the distribution is not currently taxable, and no 10% penalty applies (if you’re under 59 ½).

One-rollover-per-12-month rule

- You can do only one 60-day rollover per 12-month period, total, across all your IRAs (traditional, Roth, SEP, SIMPLE) on the “IRA to IRA” side.

- The 12-month clock starts on the date you receive the first distribution that you roll over.

- Trustee-to-trustee direct transfers do not count toward this limit; it applies specifically to 60-day, “check to you” rollovers.

Roth 401(k), 403b, and TSP Accounts

Roth employer plans are funded with after-tax money and grow tax-free. As long as it’s been 5 years since you made your first contribution to the Roth 401(k) and you are 59 ½ years old or older, you can distribute the money tax-free from the Roth. That means that if $100k is distributed from a Roth in retirement, there will be no impact on adjusted gross income. This is an important piece of the tax management puzzle in retirement. Roth allows you to manage adjusted gross income so you can stay within certain tax rates and Medicare premium brackets.

Roth IRA Accounts

Roth IRA accounts are funded with after-tax money and grow tax-free. Again, the 5-year rule applies, and it can be withdrawn tax-free at age 59 ½.

Exception for Roth IRAs to the 59 ½ rule

Roth IRAs have an exception to the 10% penalty that can be leveraged:

- Contributions come out first – the contributions you already paid taxes on will come out first, and earnings next. If your contribution is $1,000 or less, it is not taxable.

- Earnings (growth on all Roth dollars) – come out after contributions and are subject to taxes and a 10% penalty.

Example:

Sally contributed a total of $20k to her Roth IRA, and it is valued at $50k today. She is 53 years old and needs funds to cover short-term expenses. She can withdraw up to $20k from her Roth IRA tax-free because her contributions are withdrawn first.

Alternatively, if she distributes $30k, $20k will be tax-free (her contribution amount), and $10k will be taxable, plus a 10% penalty.

Sally can take advantage of a 60-day rollover to reinstate the funds in the account. Meaning, if Sally deposited the money she withdrew back into the Roth IRA within 60 days, it is treated as a tax-free rollover, and the distribution is effectively undone for tax purposes (subject to the one rollover per 12-month rule for IRA to IRA / Roth to Roth rollovers).

- You can only do one such 60-day IRA/Roth IRA rollover in any rolling 12-month period across all your IRAs; if you’ve done another 60-day IRA or Roth IRA rollover in that window, this one would not be allowed, and the 10k would be a permanent distribution.

- If you miss the 60-day deadline and don’t deposit the $30k back within 60 days, the $20k is still tax-free but can’t be redeposited. The $10k amount is subject to taxes and a 10% penalty.

Taxable Accounts

Taxable brokerage accounts invested in stocks, bonds, ETFs, mutual funds, and other investments are taxed each year on interest and dividends. These are reported on Form 1099-DIV and Form 1099-INT.

- When stock ABC issues a dividend, that adds to the amount reported on your 1099-DIV

- When a bond pays interest, that adds to the amount reported on your 1099-INT

Capital gains could apply in two scenarios.

- When you sell a stock for a gain (e.g., you buy stock xyz for $10 and sell for $30), you owe capital gains taxes (at 0%, 15% or 20% cap gains rates, depending on income for the year)

- A mutual fund passes along a capital gain realized within the fund. Because there is little control over when actively managed mutual funds disburse capital gains, there could be more tax-efficient strategies to consider for taxable accounts.

Revocable Living Trust

A revocable living trust is taxed in the same way as a taxable brokerage account, as long as the grantor is alive. When you set up a revocable living trust as a grantor, you maintain full control over the trust – by definition, it is revocable, and all income and capital gains are reported to your Social Security number.

Upon your death, the trust becomes irrevocable, and the taxes will be reported under a separate EIN.

Savings/Checking Accounts

Distributions from checking and savings accounts are tax-free; you already paid taxes on those amounts. Interest income is taxed, and a 1099-INT is issued for your checking and savings accounts.

Another Exception to 59 ½ rule – 72t exception

Rule 72(t) lets someone under 59 ½ take a series of structured withdrawals from an IRA (or sometimes a plan) without the 10% early-distribution penalty, as long as they follow strict “substantially equal periodic payment” (SEPP) rules.

Core concept

- You set up a schedule of substantially equal periodic payments (SEPPs) from the account.

- As long as you follow that schedule, the 10% penalty is waived, but the withdrawals are still taxable income from a traditional IRA.

Duration requirement

- Once started, payments must continue for the longer of:

- 5 full years, or

- Until you reach age 59 ½.

- If you start at 50, you must run it to at least 59 ½; if you start at 57, you must run it through age ~62 (five years).

Calculation methods

You must pick one of three IRS-approved calculation methods (all based on account balance, life expectancy tables, and an interest rate limit).

For purposes of this article, we will not go into the 3 ways to calculate this. Check with your financial advisor and CPA/EA to ensure you properly execute and report the 72t.

But it’s an important exception to the 59 ½ rule if you need distributions before age 59 ½.

Strategic Tax Control

Mastering the tax treatment of your retirement accounts gives you powerful control over your adjusted gross income (AGI), which directly impacts tax brackets, Medicare premiums (IRMAA), RMD timing, and even your heirs’ future tax burden. By strategically sequencing distributions—leveraging Roth basis first, timing 60-day rollovers carefully, and understanding exceptions like 72(t) or the Rule of 55—you can minimize current taxes while preserving flexibility.

Proactive planning across pre-tax, Roth, taxable, and trust accounts lets you stay in lower brackets, avoid trust-level compression, and optimize lifetime tax efficiency. Work with your advisor and CPA throughout the year, not just at tax time—strategic distributions are far more effective when executed in real time.

We want you to retire with Purpose and Clarity!

The Vocare Wealth Advisor Team

Any opinions are those of the author and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Past performance is not a guarantee of future results. Investing involves risk and you may incur a profit or loss regardless of strategy selected, including asset allocation and diversification.

Raymond James and its advisors do not offer tax or legal advice. You should discuss any tax or legal matters with the appropriate professional.

The hypothetical story is not indicative of any specific situations or client. It is presented only as an example and not intended as investment advice. Investing involved risk and there is no assurance that any investment strategy will be successful.

401(k) plans are long-term retirement savings vehicles. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty. Roth 401(k) plans are long-term retirement savings vehicles. Contributions to a Roth 401(k) are never tax deductible, but if certain conditions are met, distributions will be completely income tax free.

Contributions to a traditional IRA may be tax-deductible depending on the taxpayer’s income, tax-filing status, and other factors. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty.

Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount may be subject to its own five-year holding period. Converting a traditional IRA into a Roth IRA has tax implications. Investors should consult a tax advisor before deciding to do a conversion.

Please be aware that the early distribution penalty tax exception, substantially equal periodic payments, available via Section 72(t) of the Internal Revenue Code, is subject to very specific guidelines, and thus, various factors should be carefully considered. Investors should understand the account value (net equity and/or principal balance) could potentially be exhausted if the distributions exceed the earnings and growth of the investment(s) in the account. Also, the ability to sustain substantially equal payments can be compromised if the account is exposed to higher volatility through higher risk or growth-oriented products. Always consult the advice of an independent tax professional prior to initiating 72(t) substantially equal periodic payments.